Inflation is a crucial thing that could erode the shopping strength of your retirement savings over the years. As charges for goods and offerings boom, the price of your cash decreases, doubtlessly jeopardizing your financial safety in retirement. Understanding the impact of inflation and imposing techniques to defend your nest egg is essential for keeping your fashionable dwelling to your golden years. This article explores the outcomes of inflation on retirement savings and offers complete strategies to guard your economic future.

Understanding Inflation

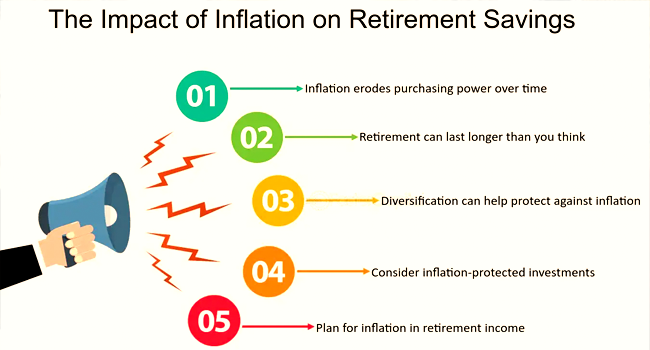

Inflation is the charge at which the overall stage of costs for goods and offerings rises, leading to a decrease in the shopping electricity of cash. It’s usually measured through the Consumer Price Index (CPI), which tracks modifications in the cost of a basket of customer items and services over the years. While moderate inflation is a normal part of a growing economic system, high or unpredictable inflation can affect your retirement financial savings.

1.How Inflation Affects Retirement Savings

Related Post

Reduced Purchasing Power: This means that the savings you have set aside for retirement might not stretch as some distance as you had deliberate.

Increased Costs of Living: Inflation affects various living costs, such as housing, healthcare, food, and utilities. As these costs boom, retirees may additionally find it tough to maintain their desired lifestyle

Erosion of Fixed Incomes: Retirees counting on constant incomes, such as pensions or annuities that do not regulate inflation, can also enjoy a decline in their actual income over time.

Investment Returns: Inflation can also affect investment returns. Even if your investments are developing, excessive inflation can lessen the actual cost of these returns.

2.Historical Context of Inflation

To hold close to the ability effect of inflation on your retirement financial savings, it’s helpful to recognize its historical context. Over the past century, inflation within the United States has averaged about three, keeping with 12 months. However, there have been periods of both excessive and low inflation:

Nineteen Seventies and Early Eighties: The U.S. Skilled high inflation rates, frequently exceeding 10%, significantly eroded savings’ shopping strength.

Nineties and Early 2000s: Inflation became very low, averaging around 2-3% in step with yr.

Recent Years: Inflation has remained modest; however, issues regarding destiny will increase due to persistent economic policies and worldwide activities.

Understanding these traits can help retirees plan for various inflation eventualities.

Strategies to Protect Your Retirement Savings

1. Diversify Your Investments

Diversification is an essential method to shield towards inflation. By spreading your investments across diverse asset instructions, you may lessen hazards and improve your capacity for returns that outpace inflation.

Key Considerations:

Stocks: Historically, shares have provided returns that exceed inflation over the long term. Investing in a different portfolio of equities can help grow your financial savings.

Bonds: While conventional bonds may be susceptible to inflation, inflation-included securities like Treasury Inflation-Protected Securities (TIPS) alter their foremost value with inflation, providing a hedge in opposition to rising prices.

Real Estate: Real property investments and Real Estate Investment Trusts (REITs) can provide earnings and appreciation capability that often keeps pace with inflation.

It can provide safety as these properties grow in price during inflationary periods.

2. Consider Inflation-Protected Securities

Treasury Inflation-Protected Securities (TIPS) are government bonds designed to guard against inflation. Advantages:

Interest Payments: Interest is paid semi-yearly and based on the adjusted importance, supplying a growing income circulation in inflationary intervals.

Government Backing: TIPS are subsidized by the U.S. Government, making them low-danger funding.

3. Invest in Dividend-Paying Stocks

Dividend-paying shares can provide a hedge against inflation, as many organizations boost their dividends over time, supplying a rising income movement that could help preserve your shopping power.

Key Considerations:

Blue-Chip Stocks: Focus on hooked-up corporations with a history of paying and growing dividends.

Dividend Growth: Look for corporations with robust basics and the potential to grow dividends.

Diversification: Ensure a diverse portfolio to lessen quarter-particular dangers.

4. Real Estate Investments

Real property may be an effective hedge against inflation as asset values and

Apartment earnings tend to boom with inflation. Investing in real estate can offer both capital appreciation and earnings, helping you preserve and develop your nest egg.

Key Considerations:

Direct Ownership: Buying rental properties can generate a regular earnings flow and admire over the years. They frequently pay excessive dividends, which can be particularly attractive to retirees.

Diversification: Include exclusive types of properties (residential, business, business) in various locations to unfold hazards.

5. Maintain an Emergency Fund

An emergency fund in a liquid, easily reachable account is essential for handling surprising costs and inflationary pressures. While this fund won’t earn high returns, it affords economic protection and flexibility.

Key Considerations:

Liquidity: Keep your emergency fund in a high-yield savings account or a cash market fund.

Size: Aim to save sufficient to cover six to twelve months of living charges, adjusting primarily based on your comfort stage and economic scenario.

6. Delay Social Security Benefits

Delaying Social Security benefits can increase your monthly bills, but they also offer more considerable, inflation-adjusted earnings in the future. Benefits increase by about 8% each year you delay taking them past your full retirement age, up to 70.

Advantages:

Higher Lifetime Income: Delaying advantages can cause better lifetime payouts, mainly if you stay longer than expected.

Inflation Adjustments: Social Security advantages are adjusted for inflation yearly, imparting safety in opposition to growing charges.

7. Consider Annuities with Inflation Protection

Annuities can offer a consistent profit stream in retirement, and a few provide inflation safety. These annuities regulate payouts based on inflation, ensuring that your shopping strength is maintained through the years.

Key Considerations:

Immediate vs. Deferred: Immediate annuities begin payouts right away, even as deferred annuities start at a destiny date.

Inflation-Adjusted Options: Look for annuities designed to modify payments based on inflation.

Fees and Terms: Be aware of the expenses and terms associated with annuities, as they can vary widely.

8. Budget for Inflation

Creating a price range that accounts for inflation permits you to control your fees and alter your spending behaviour through the years. Regularly reviewing and updating your finances guarantees you live on target despite growing charges.

Key Considerations:

Track Expenses: Monitor your spending to identify areas where you could cut expenses if necessary.

Adjust Projections: Incorporate an expected inflation price (commonly 2-3%) into your financial projections.

Flexible Spending: Prioritize crucial fees and be bendy with discretionary spending.

9. Healthcare Planning

Healthcare fees often push upward faster than widespread inflation, making planning for those retirement expenses essential. Consider long-term care insurance and fitness savings money owed (HSAs) to cover ability healthcare charges.

Key Considerations:

Health Savings Accounts (HSAs): HSAs provide tax advantages for healthcare costs, and the funds can grow tax-loose if used for qualified clinical expenses.

Medicare Planning: Understand Medicare coverage options and out-of-pocket prices to plot therefore.

10. Continual Learning and Adaptation

Staying knowledgeable about financial traits and adjusting your retirement approach as you wish is critical for coping with inflation. Regularly reviewing your economic plan with a professional allows you to adapt to changing situations.

Key Considerations:

Financial Advisor: Work with a financial guide to develop and maintain an approach that accounts for inflation.

Ongoing Education: Use reliable resources to stay up to date on financial trends, investment techniques, and retirement plans.

Regular Reviews: Conduct annual opinions of your financial plan to ensure it aligns with your desires and the cutting-edge economic environment.

11.Case Studies: Strategies in Action

Case Study 1: John and Mary’s Diversified Portfolio

John and Mary, both in their mid-60s, deliberate for inflation by diversifying their investments. They allocated their savings to shares, bonds, real estate, and TIPS. Their portfolio covered:

forty% in dividend-paying shares: Providing boom ability and consistent earnings circulate.

30% in bonds and TIPS: Offering balance and inflation safety.

20% in REITs: Giving exposure to real property without direct assets control.

10% in a high-yield financial savings account: Ensuring liquidity for emergencies.

These various methods helped John and Mary mitigate the impact of inflation whilst reaching their retirement earnings desires.

Case Study 2: Susan’s Real Estate and Annuities

A retired instructor, Susan invested in condominium residences and inflation-adjusted annuities to secure her retirement. She:

I purchased two apartment residences, generating condo earnings and appreciating costs over the years.

I bought an inflation-adjusted annuity, which provides constant earnings that are elevated with inflation.

She maintained an emergency fund, Covering surprising fees without tapping into her investments.

Susan’s strategy provided her with a stable income, protection against inflation, and peace of mind.

Case Study 3: James’s Delayed Social Security and Healthcare Planning

James, a retired engineer, centred on maximizing his Social Security blessings and planning healthcare expenses. He:

Delayed Social Security till age 70: Receiving better monthly bills.

I have purchased long-term care insurance to protect against the excessive long-term care fees.

Contributed to an HSA: Using the tax advantages to cover medical costs.

By delaying Social Security and planning for healthcare, James ensured higher, inflation-adjusted earnings and reduced his financial risk.

Conclusion

Inflation is an inevitable financial issue that could drastically impact your retirement savings and lifestyle. However, by understanding its consequences and imposing comprehensive strategies, you may shield your nest egg and maintain your monetary security. Diversifying your investments, thinking about inflation-blanketed securities, investing in real estate, keeping an emergency fund, delaying Social Security benefits, and making plans for healthcare are all effective ways to safeguard your retirement financial savings.

Knowledge and working with a financial advisor can also enhance your ability to navigate inflation and achieve a comfortable and pleasing retirement. You can ensure that your retirement financial savings continue to support your desired lifestyle throughout your golden years.